FiDA back in motion: from ambitious to workable

After months of silence, there are signs of renewed movement in the European Financial Data Access (FiDA) file. Since the trilogue negotiations stalled in June 2025, progress has been limited. The discussions between Parliament, Council and Commission did not lead to a clear final outcome. Recently, the European Commission published a new non-paper with proposed adjustments. The objective is clear: to restart the process and move towards a political agreement.

Political pressure: fewer rules, lower burden

The context in which FiDA is developing has changed. Calls for deregulation have become louder. Germany plays a key role in this. As the largest economy in the EU and one of the most influential Member States in the Council, its position has a direct impact on the feasibility of European regulation.

The position of Friedrich Merz, focused on reducing regulation and administrative burdens for companies, resonates across Europe, including in countries such as France and the Netherlands. This reflects the core criticism of FiDA: too complex, too broad and too burdensome for the market.

Germany’s stance effectively acts as a political anchor in the negotiations. Without movement from Germany, reaching agreement on FiDA is difficult to envisage.

From ambitious to workable: FiDA turns more pragmatic

The Commission’s revised approach marks a clear shift. FiDA is moving away from an ambitious and relatively heavy open finance framework towards a more pragmatic and market-oriented model.

Key elements include a narrower and less burdensome scope, reduced requirements to share historical data, greater protection of commercially sensitive data, phased and more manageable implementation, reduced bureaucracy, and more room for market-driven standards.

At the same time, tensions remain. Mandatory data sharing is still part of FiDA, which is exactly where much of the resistance lies. In addition, FiDA introduces another regulatory layer on top of existing frameworks such as PSD2 and GDPR.

What is changing?

The non-paper introduces a series of targeted adjustments to make the framework lighter and more workable.

1. Narrower Scope

The scope is reduced by excluding certain entities and datasets, such as credit rating agencies, large corporates and smaller financial firms. Further exclusions are being considered, including small insurance intermediaries. This reduces complexity and compliance burden.

2. Limited Requirements for Historical Data

Requirements to share historical data are being limited. Instead of broad datasets over long periods, a phased approach with a shorter look-back period is considered, for example two years. Terminated contracts are often excluded. This lowers costs and reduces privacy concerns.

3. Protection of Proprietary Data

Only data that has not been substantially processed falls within scope. This protects enriched or proprietary data and helps preserve competitive advantage.

4. Market-Driven Standards and APIs

The development of standards and APIs is partly delegated to the market via European standardisation organisations. At the same time, detailed EU-level obligations are reduced. This increases flexibility and reduces top-down regulation.

5. Phased Rollout Over Four Years

FiDA will be rolled out in three phases over approximately four years. Data sharing schemes are set up first, followed by mandatory data sharing. After each phase, the Commission will evaluate progress and may adjust the next phase. This lowers implementation risks and improves manageability.

6. Rejection of a Purely Demand-Based Approach

An alternative approach where data would only be shared if there is proven market demand is explicitly rejected. This prevents fragmentation across Member States and ensures that customer rights remain central.

7. The Role of Big Tech

The role of large technology companies has become a central topic. Options include restricting access to data or limiting licensing. There is no consensus yet, but the issue is clearly on the table.

8. Streamlined Licensing

The licensing process for financial information service providers is simplified, including reuse of existing PSD2 information and fewer duplicate procedures. This reduces administrative burden.

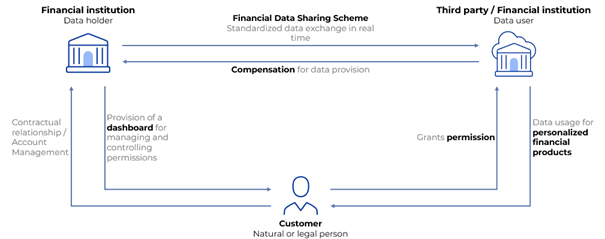

9. Data Holders as Data Users

An important principle remains unchanged. Data holders can also access data from others, subject to customer consent. This means traditional financial institutions become both data providers and data users.

Strategic implications for financial institutions

Although the revised FiDA model is becoming lighter, the strategic implications remain significant. FiDA is not simply a compliance exercise. It represents another major step towards data-driven financial ecosystems.

Even though FiDA is still evolving politically, financial institutions should already begin assessing their readiness.

Key focus areas include:

- reviewing enterprise data architecture,

- assessing API maturity and interoperability,

- strengthening consent and identity management,

- evaluating data governance frameworks,

- and identifying proprietary versus shareable datasets.

The revised framework also creates potential opportunities like new data-driven services, personalised financial products and future monetisation opportunities around customer-consented data access.

Early preparation can help firms reduce future implementation costs, avoid fragmented transformation initiatives and position themselves strategically as Open Finance ecosystems mature.

Conclusion: FiDA is not abandoned, but it is being recalibrated. The European Commission is moving towards a more pragmatic approach that prioritises feasibility and political support.

The revised framework significantly reduces complexity and implementation burden for market participants. However, the core principle of mandatory, standardised financial data sharing remains unchanged.

This means the strategic direction of travel is still clear: Europe continues to move towards Open Finance.

Institutions that treat FiDA purely as a compliance topic risk missing the broader structural transformation towards interoperable.

As the regulatory landscape continues to evolve, firms should use the current transition phase to assess their strategic positioning, strengthen their data capabilities and prepare for future Open Finance operating models.

At X Group, we support financial institutions in translating regulatory change into actionable business and technology strategies – from data and API readiness assessments to Open Finance target operating models and implementation roadmaps.

Bei Thede Consulting unterstützen wir als Teil der Projective Group Finanzinstitute dabei, regulatorische Veränderungen in umsetzbare Geschäfts- und Technologiestrategien zu überführen – von Data- und API-Readiness-Assessments bis hin zu Open-Finance-Target-Operating-Modellen und Implementierungs-Roadmaps.

Frequently Asked Questions about FiDA (FAQ)

What is FiDA (Financial Data Access)?

FiDA stands for Financial Data Access and refers to an EU regulatory framework designed to govern access to and sharing of financial data. The goal is a European Open Finance ecosystem in which customers can share their financial data with their consent.

What is changing about the FiDA regulation in 2025/2026?

The European Commission is realigning FiDA in a more pragmatic direction: a narrower scope, reduced requirements for historical data, stronger protection of proprietary data, market-driven standards, and a phased introduction over approximately four years.

How does FiDA differ from PSD2?

While PSD2 primarily governs access to payment account data, FiDA extends data access to a significantly broader range of financial products — such as savings, investments, insurance, and loans.

What should financial institutions do now?

Institutions should assess their data architecture, API maturity, consent and governance processes at an early stage in order to reduce implementation costs and position themselves strategically in the Open Finance market.

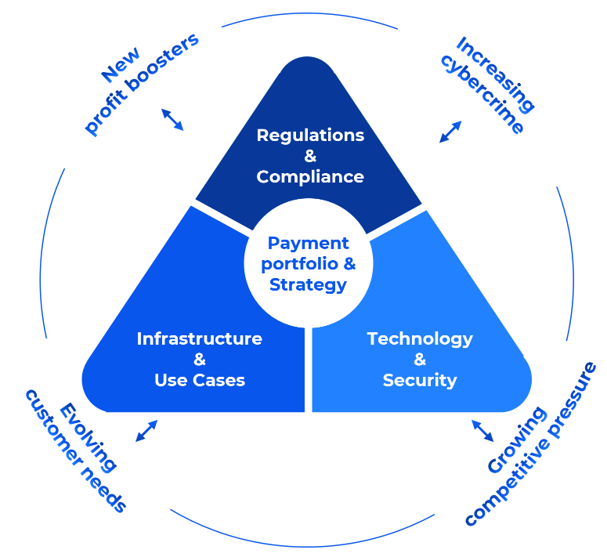

We translate complexity into strategy: Our Payment 360° Workshop

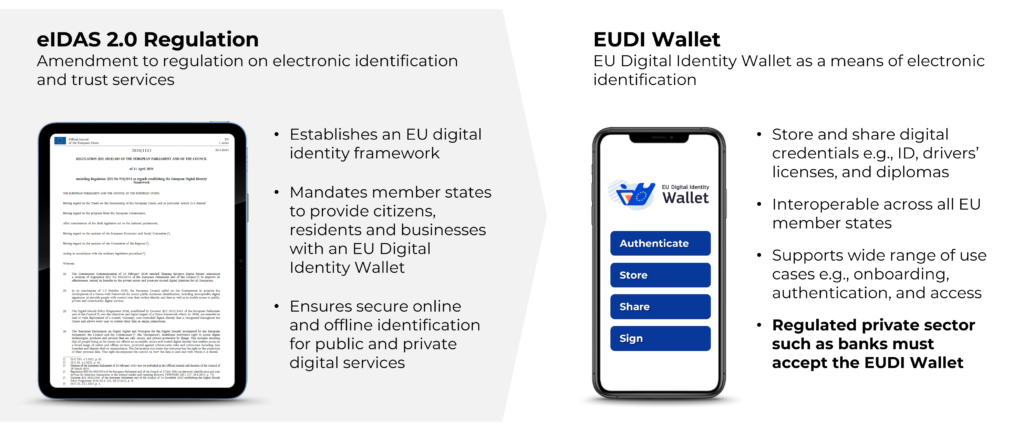

FiDA is part of our Payment 360° Workshop alongside current payment topics such as the digital euro, EUDI Wallet, and PSD3. The focus is on finding concrete answers: Which payment developments are truly relevant to your portfolio? How do you evaluate different scenarios and timelines? And what strategic fields of action can be derived from them? The format: half-day, focused on your specific situation, with an outside-in perspective rather than theory. The goal: a clear assessment of market developments in the context of your current portfolio and ambition level — so that complexity becomes an actionable strategy.

Eike Maybaum

Carolin Peters